Investing Under The Trifecta Of War, Recession, And Inflation

Russia's invasion of Ukraine has now continued for month with no end in sight. The destruction in Ukraine is incredible to see and understand, but what is clear is now a distaste for investing in Russia that likely will continue, regardless of the outcome, for the next decade at minimum. Putin has single-handedly erased the progress that Russia has made over the last three decades of its integration into the world's economy. There has always been a risk to investing in Russia, but it had become acceptable, but now with so many large corporations pulling out, putting at great risk billions of dollars of investment, its not likely they will return anytime soon.

The pall of fear overhanging global markets from the Ukraine war has somewhat dissipated as it has become more clear that its impact is increasingly isolated to Europe and energy supplies. China has made it increasingly clear, that they do not want to be overly involved and definitely not in aggressively supporting Putin's side. It is a shame that China not stand up for what most of the world agrees is an act of terrorism and an unjustified war, particularly against civilians. For the U.S., Russia was a source of oil imports accounting for an estimated 7% of daily consumption. I expect this will be sourced elsewhere, and although it may lead to higher oil prices, it won't cause series supply disruptions that could cause other cascading issues on our economy.

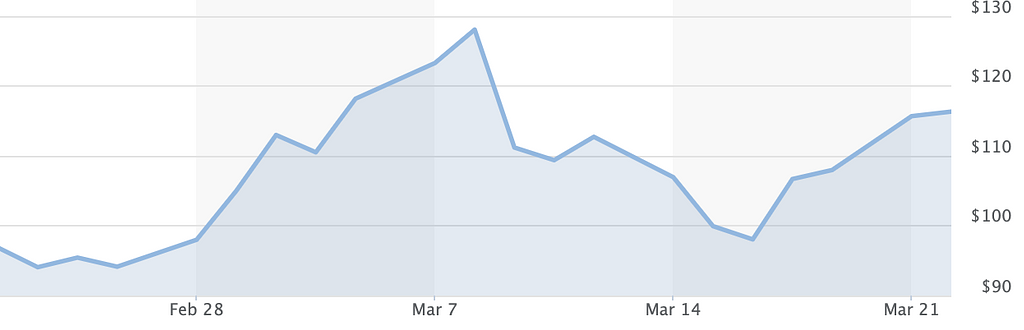

Oil prices are now off their peak hit in early March with Brent oil contracts at $127, and hover around $116. This is up sharply from the average $92-$96 range we were seeing in February. This will impact the U.S. economy, particularly in transportation and manufacturing, both big consumers of energy, and we will see it with higher prices. The Federal Reserve will be raising rates this year we can hope will temper demand for goods and prices.

Brent Continuous Contract Prices

All in all though, I don't see significant changes in inflation at this point. Energy prices will stabilize, but at least for airlines, demand will be significantly higher, even with higher ticket prices, which will result in their return to revenue growth and profitability. My favorites remain as Delta (DAL) and Southwest (LUV), as both are position the best financially, capable of weathering any market turmoil due to their low debt levels and high cash availability. In fact, both airlines have actually been expanding and likely will come out of the COVID and energy prices escalation period, stronger than before.

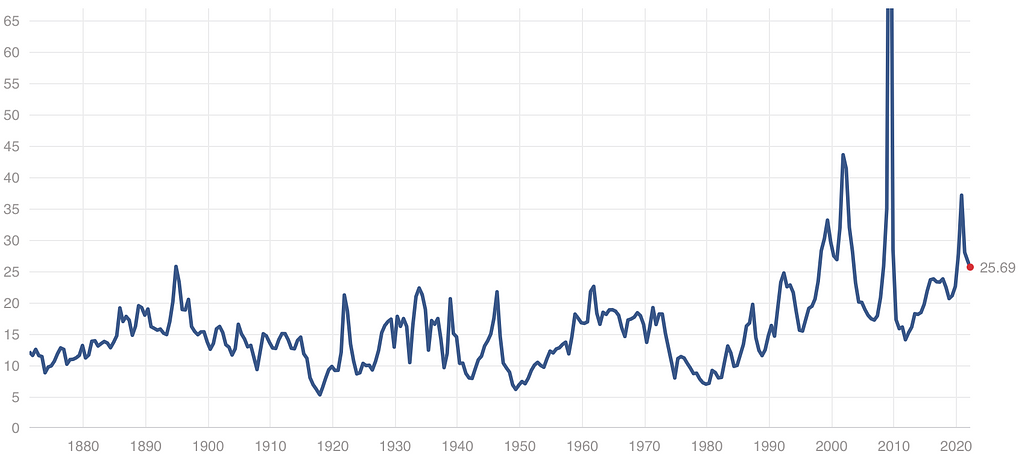

The market has been recovering, after sharply deflating over the last six months and is only slightly higher than the long term average. The S&P 500 price-to-earnings is now at 25.69, down from 38 a year ago, and for the Dow Jones Industrial Average, the average is at 19.44, down from 33 a year ago. Albeit these averages are still not as low as I'd like, the levels are a lot more comfortable to be at than where we were a year ago.

S&P 500 PE Ratio (LTM)