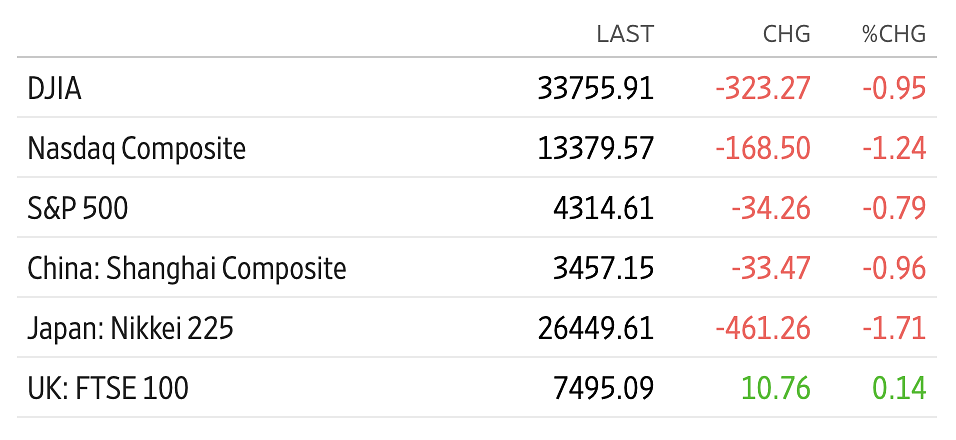

Russia's move into the Ukraine today is raising the specter of war--a geopolitical risk that depending on its scale, and amongst many other dangers, roil financial markets and impact investment returns. I won't try to over-analyze the actions and potential impact directly in the region, as doing so is fraught with so many outcomes, with such a small probability of being accurate in its determination. Instead, we can assess the risk through a spyglass on our companies and how they might be exposed, which in fact, those conclusions may largely be applied to the U.S. economy, and U.S. companies.Screen Shot 2022-02-22 at 8.55.40 AM.png75.3 KB Markets are smart and often early indicators of where things are going, and interestingly, markets have mostly brushed off today's actions. Overnight, when the news broke that Russia was making moves into Ukraine, the UK's FTSE 100 stock index was up 0.14%, Japan's Nikkei 225 and China's Shanghai Composite were both down slightly by 1.71% and 0.96%, respectively. More directly, as this incursion is already leading to increased shipping costs for commodities, and supply interruptions, commodity prices are up modestly, with oil by 1.8%, gold up 0.2%. Natural gas is up more sharply at 11% in Europe, as supply issues are significant considering that Germany has put a halt on any further development of a the Russian-German Nord Stream 2 gas pipeline.

Ukraine, Russia and eastern Europe is not a significant risk to most U.S. companies. Earnings season is over and was mostly good overall and particularly strong for most value-oriented stocks, which is our focus. Does Russia's action pose a greater risk that we should move to avoid? It's hard to conclude that doing so would be wise in the case of Russia. There are greater unknowns that we are facing now, such as inflation, the Federal Reserve and interest rates, employment and China. These issues are imperiling returns, although in total, they still don't outweigh the strength of the U.S. economy, and technology companies in particular.

I think positioning and being selective is still the playbook. Value stocks, which I recognize are harder to find, and cash, to buy on any big dips, are attractive.